On April 1, 2019, the U.S. Small Business Administration’s new version of environmental policies and procedures took effect (SOP 50 10 5(K)). In a timely track that opened the June Environmental Bankers Association conference in Philadelphia, Eric Adams, chair of the SBA’s Environmental Committee, shared a complete list of the latest revisions and clarifications to the SOP, along with the background behind each change. Environmental professionals who support the SBA’s 7(a) and CDC lending programs would do well to review a list of common errors found in SBA loan submittals at the end of this brief. Below, with permission, are highlights from Adams’ presentation:

Changes to SOP 50 10 5, Environmental Policies and Procedures

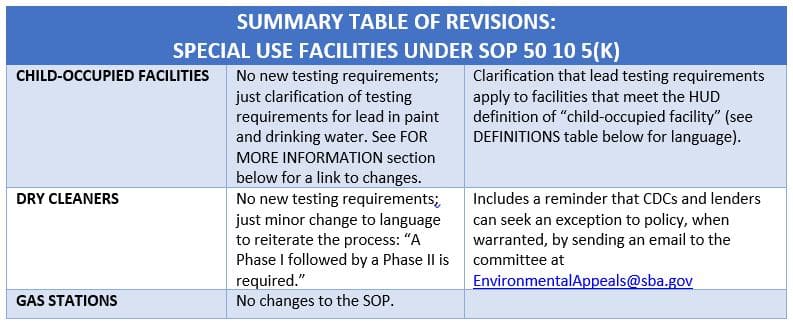

Revisions to the section on Special Use Facilities include:

Day Cares, Nursery Schools, Etc.

Testing for lead in paint and drinking water at day care centers, nursery schools and related businesses at loan origination has been an SOP requirement for over 10 years. In response to questions the SBA received from stakeholders, particularly environmental professionals, as to what testing protocols should be followed, the new version K adds a bit of clarification—but no new testing requirements. CDCs and lenders have also asked about whether particular facilities occupied by children needed testing (based upon hours of occupancy, etc.), so the new SOP also adds a new definition of “Child-Occupied Facility”—one that is consistent with the HUD definition (see table).

Dry Cleaners

No new testing requirements have been added, but the SBA did include clarification of policy regarding the need for Phase II ESAs. Under the previous version of the SOP, in most situations where dry cleaning operations occurred at the property (current or historical), lenders have been required to hire a qualified environmental professional to conduct a Phase I ESA, followed by a Phase II investigation. The new SOP acknowledges that there are cases where a new Phase II ESA may not be necessary. For example, if a Phase II was previously performed on the property and is available—and if no dry cleaning operations took place after the Phase II was performed—a lender or CDC may submit a request to the committee to review documentation and seek an “exception to policy,” if warranted.

Gas Stations

Version K does not reflect any revisions/clarifications to this section.

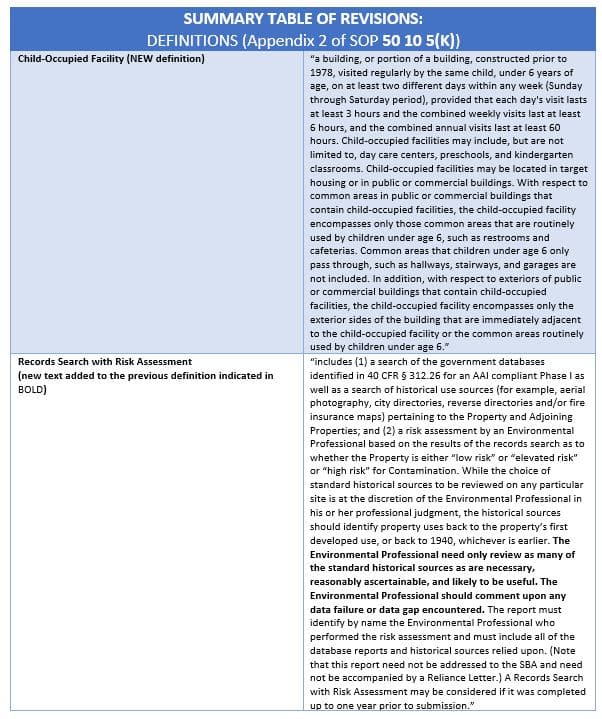

Definitions Section (Appendix 2)

In addition to adopting the HUD definition of child-occupied facility noted above, SBA also added a clarification re: historical sources to the definition of “Records Search with Risk Assessment” based on inquiries from the field:

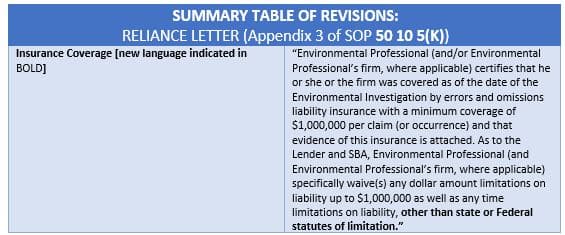

Reliance Letter (Appendix 3)

In response to feedback from environmental professionals that they could be exposed to unlimited, open-ended liability with CDCs, lenders and SBA were they to execute SBA’s template reliance letter, the new version K adds a clarifying phrase to alleviate those concerns:

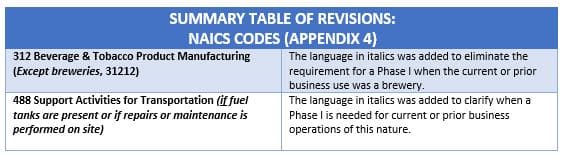

NAICS Code Changes (Appendix 4)

The NAICS code list in Appendix 4 is important because if a property’s current and known prior uses match a NAICS code for an environmentally sensitive industry identified in Appendix 4, the Environmental Investigation must begin with a Phase I ESA by a qualified environmental professional, regardless of the amount of the loan. Version K makes two adjustments to the existing industries on the list:

Believe it or not, the microbrewery craze necessitated this change. Demand for loans on microbreweries is sufficiently high that the SBA Environmental Committee was receiving numerous requests for an exception to policy requiring a Phase I ESA on brewery properties. Based on complete reviews of all environmental reports provided with these requests—and due to the minimal environmental risks associated with brewery operations, the SBA has granted waivers in every instance. As a result, SBA is making this change to policy to exempt breweries from the Phase I ESA requirement that applies to other beverage and tobacco operations under NAICS 312.

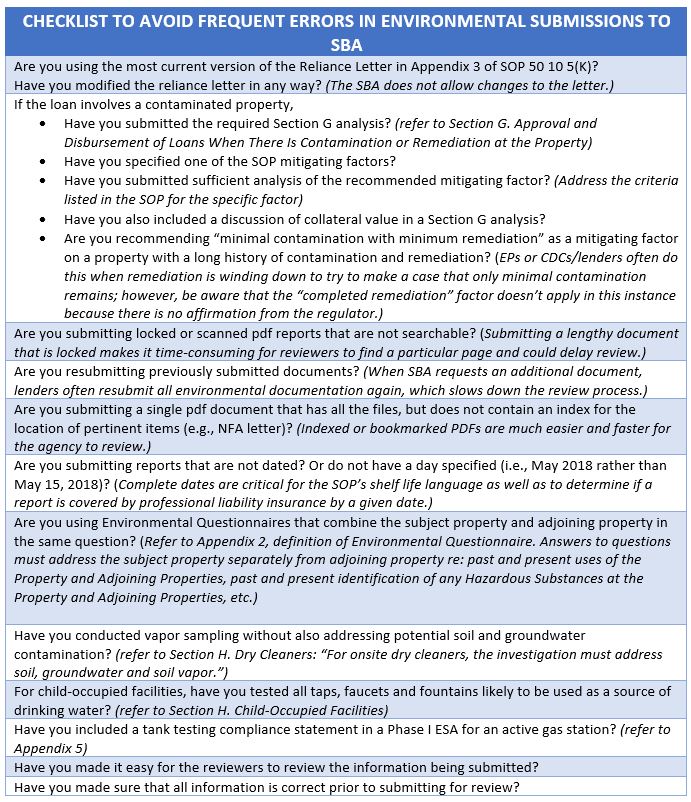

Common Errors Related to Environmental Submissions to SBA

The SBA reviews thousands of environmental submissions from lenders and CDCs. During his presentation, Adams shared some of the most common pitfalls that the agency encounters. Whether you are a lender/CDC or an environmental professional, review this checklist to ensure a timely review:

Exceptions to SBA’s Environmental Policies & Procedures

“It’s a two-way street.” Adams emphasized SBA’s commitment to “ensuring that adequate environmental due diligence is conducted without requiring that lenders or CDCs do excessive due diligence.”

The agency can be somewhat flexible when it comes to implementing the environmental policies and procedures. When warranted, lenders/CDCs have the option of requesting that the environmental committee consider an exception to policy. Any requests for exceptions to policy, technical questions, clarifications, appeals or general feedback, simply email the committee directly at EnvironmentalAppeals@SBA.Gov. Additionally, the committee also welcomes suggestions for improvements to the environmental guidelines at this email address.

FOR MORE INFORMATION

- The current SBA SOP 50 10 5(K) policy is available here, effective April 1, 2019, and applies to all applications received by SBA on or after that date.

- For a comparison of the language in version J vs. version K, specifically with regard to Special Use Facilities (i.e., child-care facilities, dry cleaners), refer to this EDR® brief from February highlighting key areas of change: U.S. SBA RETURNS FROM SHUTDOWN WITH A NEW SOP 50 10 5, EFFECTIVE APRIL 1ST.

- Questions on SBA’s Environmental Policy should be directed to local SBA counsel for the area where the Property is located.

- Download EDR®’s updated SBA process flow diagram (step-by-step instructions for conducting environmental due diligence on SBA loans), or to get information on our LoanCheck RSRA solution.